💼 Life Insurance Agent Commission Calculator

Estimate your first-year commissions, renewal income, and override earnings with real industry rates

⚡ Quick Presets

🧮 Commission Inputs

DISCLOSURE: This post may contain affiliate links, meaning when you click the links and make a purchase, I receive a commission. As an Amazon Associate I earn from qualifying purchases.

💰 Your Commission Estimate

📊 Commission Rate Reference by Policy Type

1st Year

1st Year

1st Year

1st Year

Renewal

Renewal

Renewal

(GA Level)

📋 First-Year Commission Rates by Agent Level

| Policy Type | Captive Agent | Independent (IMO) | General Agent (GA) | MGA |

|---|---|---|---|---|

| Term Life 10-Yr | 40–55% | 55–70% | 70–80% | 80–90% |

| Term Life 20-Yr | 45–60% | 60–75% | 75–85% | 85–95% |

| Term Life 30-Yr | 45–65% | 65–80% | 80–90% | 90–100% |

| Whole Life | 50–70% | 80–100% | 100–115% | 110–120% |

| Universal Life | 50–65% | 75–90% | 90–105% | 100–110% |

| IUL | 55–70% | 80–95% | 95–110% | 105–115% |

| Final Expense | 60–75% | 80–100% | 100–115% | 110–120% |

| Graded Benefit | 55–70% | 75–95% | 90–105% | 100–110% |

| Variable Life | 40–55% | 60–80% | 80–95% | 90–100% |

🔄 Renewal Commission Rates (Years 2+)

| Policy Type | Year 2 | Year 3 | Years 4–5 | Years 6–10 | Year 11+ |

|---|---|---|---|---|---|

| Term Life | 3–5% | 3–5% | 3–5% | 2–3% | 1–2% |

| Whole Life | 5–8% | 5–8% | 5–8% | 4–6% | 3–5% |

| Universal Life | 3–6% | 3–6% | 3–6% | 2–4% | 1–3% |

| IUL | 4–7% | 4–7% | 4–7% | 3–5% | 2–4% |

| Final Expense | 5–8% | 5–8% | 5–8% | 3–5% | 2–4% |

| Variable Life | 3–5% | 3–5% | 3–5% | 2–3% | 1–2% |

🧮 Annual Earnings Projection — 10 Policies Example

| Scenario | Avg Premium | FY Comm Rate | Year 1 Earnings | Year 3 Renewals |

|---|---|---|---|---|

| Part-Time (10 policies) | $1,000 | 65% | $6,500 | $400 |

| Full-Time (30 policies) | $1,200 | 70% | $25,200 | $1,440 |

| Top Producer (60 policies) | $1,500 | 85% | $76,500 | $4,500 |

| GA Overrides (100 policies) | $1,200 | 10% | $12,000 | $3,600 |

| Final Expense Specialist (40 policies) | $600 | 95% | $22,800 | $1,440 |

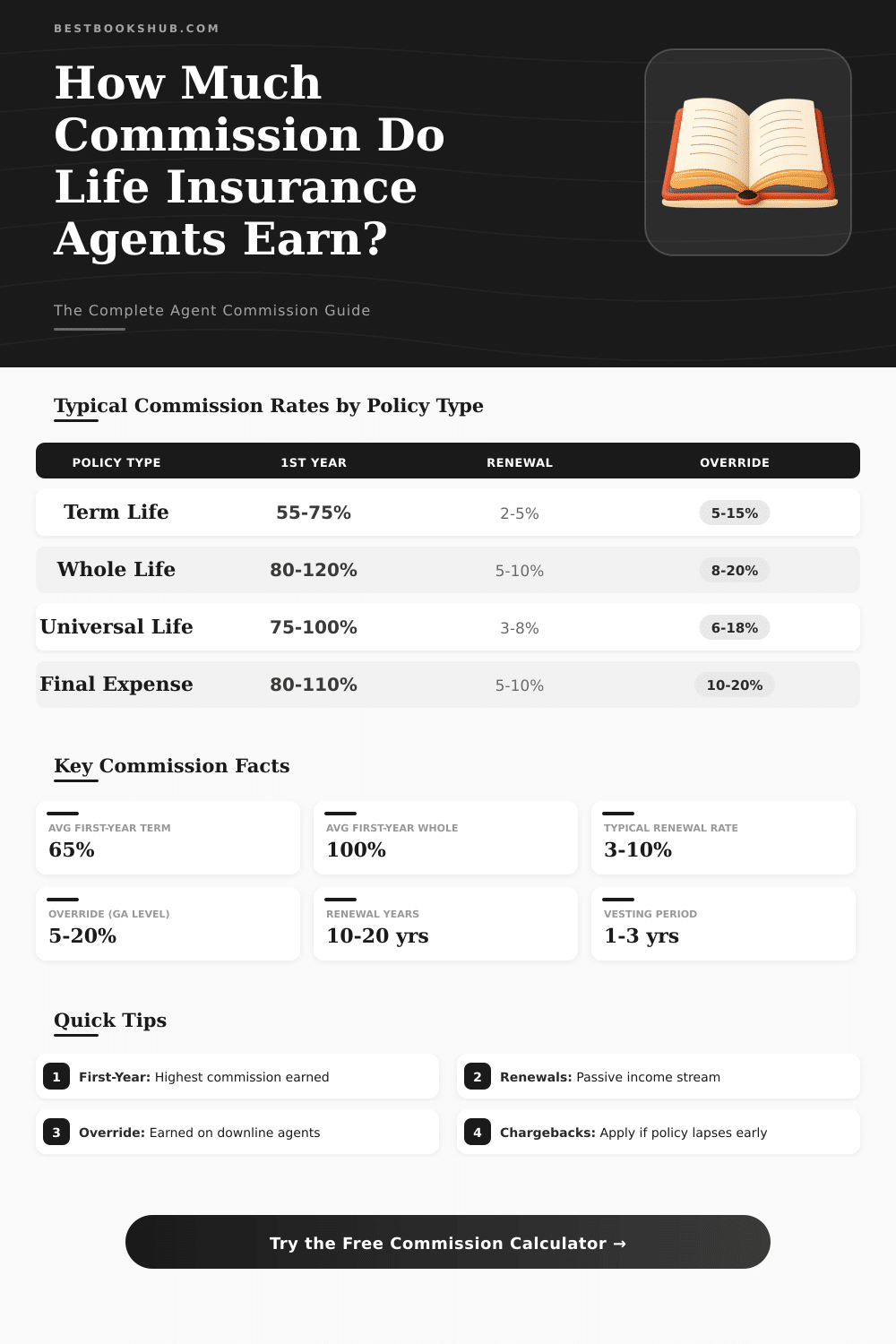

When you sell life insurance, you get the biggest part of your income through commissions. When they sell policies, they receive a big first payment. That proportion ranges between 40% and 100% of the yearly feature, what represents the fund for the yearly salary of the insured.

Some contracts even reach 120% until 180% from that same yearly feature. The precise ratio depends on several factors.

How Life Insurance Agents Get Paid

The height of commissions changes according to the sales channel depending on that, do the agents are tied or independent. It also varies according to the schedule of commissions of the company and the kind of sold product. Agents, that work in agency, commonly start with low levels, if they only involve themselves about signing and do not bring clients.

When one does both selling and signing, opens way to bigger profit margins.

The kind of life insurance product plays a big role. Here products like variable universal life insurance, variable insurance and universal life insurance tend to give high margins to the insurance company. Hence they offer high life insurance agent commission rates to the agents.

Whole life insurance commonly is seen as the base of life insurance companies, like bread and butter. Because commissions form a share of the features, the agents have reason to promote policies with biggre payments, for instance permanent life insurance. Those contracts usually ensure coverage for whole life and include a cash value part, that grows interest according to the time.

Life insurance usually gives bigger first commission than property insurance and car insurance. Health insurance, on the other hand, bases itself more on continuous commissions. First commissions are one-time payments, that one wins during sale of policies, and they are most common for term life insurance, life insurance and annuity policies.

There are also renewal commissions. For whole life insurance, those can reach until 7.5% of the feature during the next nine years. Top sellers receive 100% of the feature as commission in the first year, later typical 2% until 5% of the second until fourth year.

Renewal commissions affect more strongly the long-term incomes then the first commissions.

Some agents offer 40% until 50% or more in commission, but that covers expenses like overhead, CRM and automatic calculators. One advises independent life insurance agents to not accept nothing under 90% of the yearly annual feature. Commissions for whole life insurance are calculated according to the annual feature, not the total listed fund, and the proportion is much more low than the standard 55% for usual wholelife insurance.

Selling life insurance is a challenge. Refusals form part of the work. It is a numbers game, and even reaching a client for a chat does not guarantee equal chance for commission.

Life insurance also hardly sells, because many folks do not feel they need it. Companies experienced high agent cost during decades. It is good to have clear strategies when one enters that branch.