💼 Insurance Agent Commission Calculator

Estimate your first-year and renewal commissions across all major policy types

First Year

New Business

Commission

Commission

First Year

New Business

Per Policy (CMS)

Commission

| Policy Type | First-Year Rate | Renewal Rate | Avg Annual Premium | Est. First-Year Comm. |

|---|---|---|---|---|

| Term Life | 40–90% | 2–5% | $600–$900 | $240–$810 |

| Whole Life | 80–120% | 5–10% | $1,000–$2,000 | $800–$2,400 |

| Universal Life | 60–100% | 3–8% | $1,200–$3,000 | $720–$3,000 |

| Auto Insurance | 10–15% | 8–12% | $1,200–$1,800 | $120–$270 |

| Homeowners | 10–20% | 8–15% | $1,000–$1,500 | $100–$300 |

| Health (ACA) | 3–8% | 2–4% | $3,600–$6,000 | $108–$480 |

| Disability | 40–70% | 5–10% | $1,500–$3,000 | $600–$2,100 |

| Fixed Annuity | 3–8% | 0–1% | $25,000–$100,000 | $750–$8,000 |

| Commercial P&C | 10–20% | 8–15% | $5,000–$15,000 | $500–$3,000 |

| Medicare Advantage | $20–$36/policy | $20–$36/policy | $0 to client | CMS flat fee |

| Policy Type | Year 1 | Year 2 | Year 3 | Year 4+ |

|---|---|---|---|---|

| Term Life | 40–90% | 5% | 3% | 2% |

| Whole Life | 80–120% | 10% | 8% | 5% |

| Auto Insurance | 10–15% | 10% | 10% | 8–12% |

| Health (ACA) | 3–8% | 3–4% | 3–4% | 2–4% |

| Disability | 40–70% | 10% | 7% | 5% |

| Commercial P&C | 10–20% | 12–15% | 12–15% | 10–15% |

| Agent Level | Override Rate | Production Requirement | Annual Bonus Potential |

|---|---|---|---|

| New Agent | 0% | None | $0 |

| Associate Agent | 3–5% | $50K premium/yr | $1,500–$5,000 |

| Senior Agent | 5–8% | $100K premium/yr | $5,000–$15,000 |

| Agency Owner / MGA | 8–15% | $250K+ premium/yr | $20,000–$50,000+ |

| IMO / FMO Level | 10–20% | $1M+ premium/yr | $100,000+ |

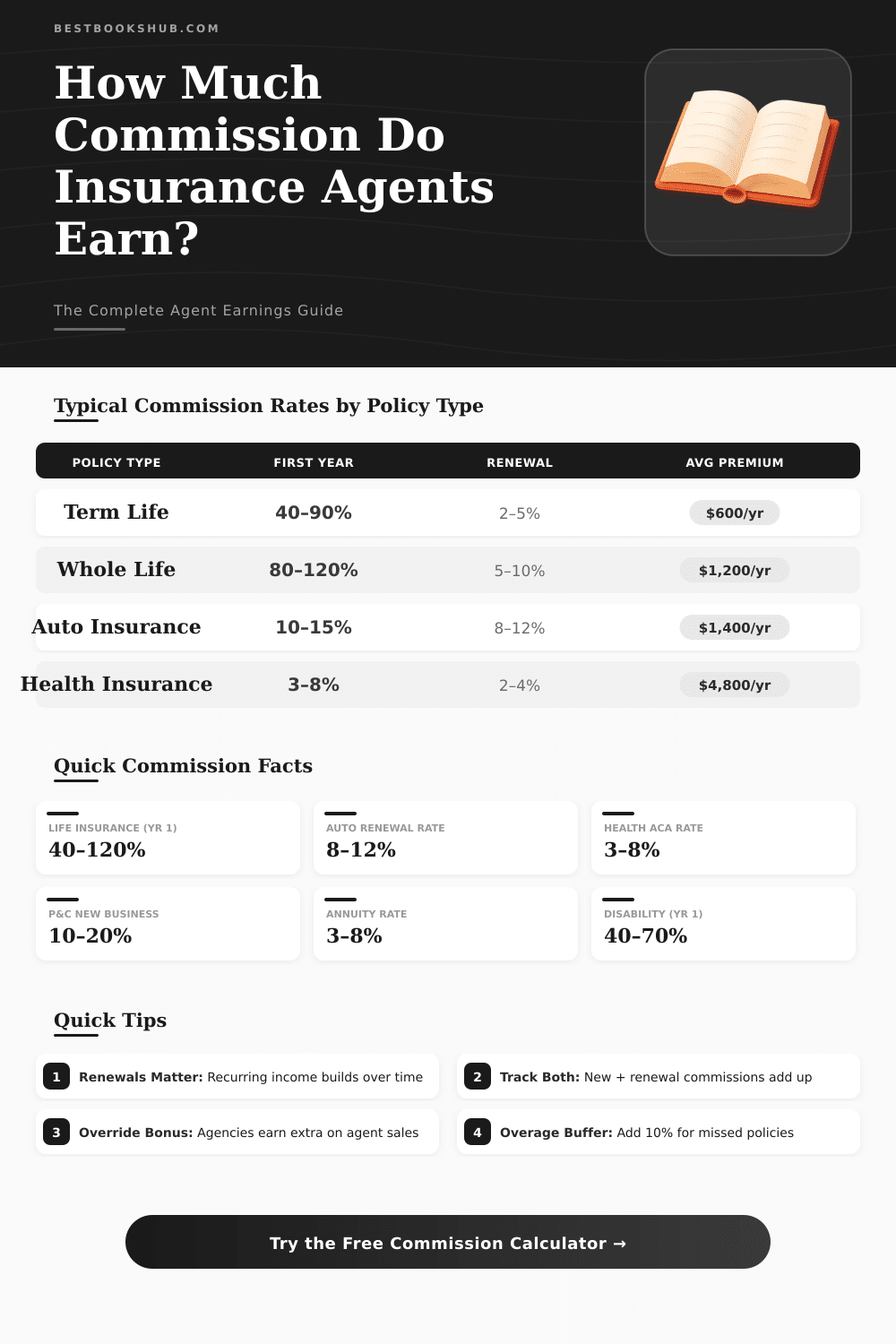

Life insurance agents often earn 80–120% of the first-year premium upfront, but renewal commissions drop to 5–10%. Building a renewal book is key to stable long-term income.

Medicare Advantage commissions are set by CMS (Centers for Medicare & Medicaid Services) as flat dollar amounts per enrollment, not as a percentage of premium. Rates are updated annually.

Insurance agents receive income through commissions. Insurance Agent Commission is made up of the part of the annual payment that the customer pays, and that goes to the agent or to the producer. Every insurer sets the exact percentage for his own products.

DISCLOSURE: This post may contain affiliate links, meaning when you click the links and make a purchase, I receive a commission. As an Amazon Associate I earn from qualifying purchases.

The clients never pay those commissions separately, because they are already included in the annual payment.

How Insurance Agents Get Paid

Here is an easy sample to show that. Assume that a policy costs 1 000 dollars yearly, and the commission rate matches 10 percent; then the agent receives 100 dollars for that sale. Usually the commission levels adjust according to various factors, for example the kind of insurance policy, the company itself and the terms of the contract between agent and insurer.

Various ways exist to pay agents. Licensed insurance agents can receive hourly pay, fixed salary, commissions, bonuses or a mix of those. For starting agents, one of the most important choices is whether to accept a position with salary and bonuses, or work purely on 100-percent commission.

Captive agents work only for one single insurer. From that company they receive a fixed salary, which guarantees stable income, regardless of the sold policies. Beyond that, they can get commission income and bonuses, that depend on the whole performance of the company.

Independent agents offer products from several insurance companies. Because they are not employees there, they depend on commission percentages. Such independent agents commonly reach up to 15 percent from the annual payments for new policies in personal lines, and from 2 to 15 percent for renewals.

Commonly the agency itself receives the commission from the insurer first. In the field the standard rate for agencies is about 10 percent. Insurers can give to agencies between 10 and 20 percent for new deals, and from 10 to 18 percent for renewals.

Later the individual agent in the agency receives a agreed portion, usually between 40 and 60 percent from that total. Some agencies offer there agents from 50 to 90 percent.

The size of commissions depends also on the insurance type. For personal lines, like car or home insurance, the percentages usually stay low. Commercial insurance on the other hand delivers higher incomes.

Products with cash value and investments give the maximum commissions, sometimes from 10 to 55 percent. Ongoing life insurance, like whole life policy, normally does not build worth in the first one or two years, because of the commissions and other bonuses.

Agents are pushed to sell policies with bigger annual payments, because the commissions form part of those amounts. One commonly calls “building a book of business” the process of growing the client base. That creates ongoing income for the company and permanent commissions for the agent.

During retirement, an agent can hand over his clients to another, against part of the commissions, that one wins from them for some years. Insurance Agent Commission levels adjust commonly every year, and the relations between insurers, agencies andagents form a complex web of different terms.