💰 Mortgage Agent Commission Calculator

Estimate your earnings per deal and monthly income based on loan amount, basis points & broker split

| Loan Amount | Gross Commission | Agent Earns (80%) | Monthly (5 deals) |

|---|---|---|---|

| $200,000 | $2,000 | $1,600 | $8,000 |

| $300,000 | $3,000 | $2,400 | $12,000 |

| $400,000 | $4,000 | $3,200 | $16,000 |

| $500,000 | $5,000 | $4,000 | $20,000 |

| $600,000 | $6,000 | $4,800 | $24,000 |

| $750,000 | $7,500 | $6,000 | $30,000 |

| $1,000,000 | $10,000 | $8,000 | $40,000 |

| $1,500,000 | $15,000 | $12,000 | $60,000 |

| Broker Split Model | Agent Keeps | On $4,000 Gross | Annual (60 deals/yr) |

|---|---|---|---|

| 60/40 (New Agent) | 60% | $2,400 | $144,000 |

| 70/30 | 70% | $2,800 | $168,000 |

| 75/25 | 75% | $3,000 | $180,000 |

| 80/20 (Standard) | 80% | $3,200 | $192,000 |

| 85/15 | 85% | $3,400 | $204,000 |

| 100% (Desk Fee) | 100% | $4,000 | $240,000 |

| Outstanding Balance | Trailer (20 bps/yr) | Agent @ 80% | After 5 Years |

|---|---|---|---|

| $500,000 | $1,000/yr | $800/yr | $4,000 |

| $1,000,000 | $2,000/yr | $1,600/yr | $8,000 |

| $2,500,000 | $5,000/yr | $4,000/yr | $20,000 |

| $5,000,000 | $10,000/yr | $8,000/yr | $40,000 |

| $10,000,000 | $20,000/yr | $16,000/yr | $80,000 |

| $20,000,000 | $40,000/yr | $32,000/yr | $160,000 |

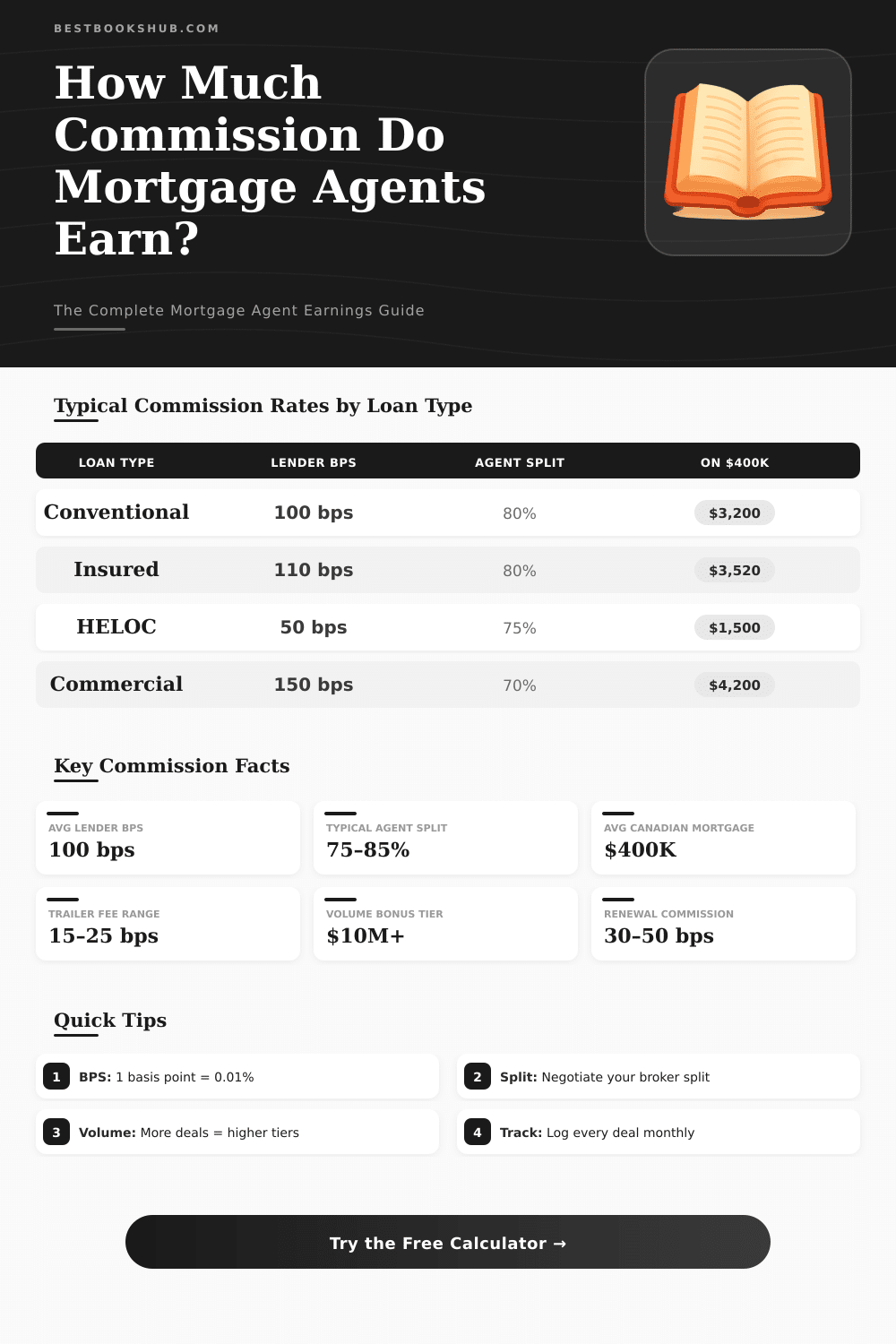

Mortgage agents receive income chiefly by means of commissions. The lender commonly delivers to the agent part of the mortgage value because of bringing in clients. That income usually ranges between 1% and 2% of the whole amount of the loan at closing.

DISCLOSURE: This post may contain affiliate links, meaning when you click the links and make a purchase, I receive a commission. As an Amazon Associate I earn from qualifying purchases.

On average they require around 2.25% for every deal. The laws of the federal government limit the maximum at 3% from the whole loan amount.

How Mortgage Agents Get Paid

The mortgage agent commission rate normally equals 2 percent, even so it adjusts according to factors like the trouble of the loan. At big banks, loan officers receive basic pay together with bonuses for reaching targets, of 0.25% until 0.5% from the loan amount. An officer for mortgage loan can reach of 0.4% until 1.5% of the amount.

For a loan of one million dollars, that matches to 4,000 until 15,000 dollars in income.

Almost all agents for mortgages depend on percentages from the loan amount. Agents of mortgages must share their commission with the firm, but they mostly keep at least 80 percent or even more. The split between the officer for mortgage loan ranges from 20% until 80%, according to there role in the deal.

Some receive according to percentages, while others base on spots.

A model with salary and commissions is more spread in big companies for mortgages and in banks. It gives basic income as security, while one builds clientele. The basic payment is less than in a purely commission system, but the commissions grow for each closed loan.

Some officers with high impact indeed reach under 1% forevery deal.

Agents for mortgages can ask a fee, receive commission from lenders or combine both for their help. Even so, reforms after the mortgage emergency introduced rules: one can pay them only from one side, either the client or the bank, not both in one same case. When the client pays directly to the agent, they can discuss the rate.

Here the client receives the basic price without extras and pays the agent directly up front.

A mortgage lender that shares commissions or gives extra guides to agents of properties breaks federal and state laws. Although, some agents get extra money by means of fees for extra advice, hiring lawyers, actuaries or agents of farms. When one works with a professional for mortgages, the fee or mortgage agent commission is paid either by the lender or by the bank.

These payments form part of the closing costs and happen during the closing. If the loan fully gets repaid, the agent does not receive any commissions from it.

An important thing to know is that agents sometimes have monetary reason to attach a loan to a particular lender. A less known bank maybe offers double the usual commission, what can cause conflict of interests for unusual lenders that require special support.