💹 Mutual Fund Agent Commission Calculator

Estimate trail & upfront commissions on AUM for mutual fund distributors & ARN holders

| AUM (₹) | Trail 0.25% / yr | Trail 0.50% / yr | Trail 0.75% / yr | Trail 1.00% / yr |

|---|---|---|---|---|

| ₹1,00,000 | ₹250 | ₹500 | ₹750 | ₹1,000 |

| ₹5,00,000 | ₹1,250 | ₹2,500 | ₹3,750 | ₹5,000 |

| ₹10,00,000 | ₹2,500 | ₹5,000 | ₹7,500 | ₹10,000 |

| ₹25,00,000 | ₹6,250 | ₹12,500 | ₹18,750 | ₹25,000 |

| ₹50,00,000 | ₹12,500 | ₹25,000 | ₹37,500 | ₹50,000 |

| ₹1,00,00,000 | ₹25,000 | ₹50,000 | ₹75,000 | ₹1,00,000 |

| Year | AUM @ 12% growth | Annual Trail (0.75%) | Cumulative Trail |

|---|---|---|---|

| Year 1 | ₹10,00,000 | ₹7,500 | ₹7,500 |

| Year 2 | ₹11,20,000 | ₹8,400 | ₹15,900 |

| Year 3 | ₹12,54,400 | ₹9,408 | ₹25,308 |

| Year 5 | ₹15,73,519 | ₹11,801 | ₹47,222 |

| Year 7 | ₹19,73,823 | ₹14,804 | ₹72,441 |

| Year 10 | ₹31,05,848 | ₹23,294 | ₹1,40,612 |

| Monthly SIP | AUM After 3 Yrs | AUM After 5 Yrs | Annual Trail @ 0.75% |

|---|---|---|---|

| ₹5,000 / mo | ₹2,19,000 | ₹4,05,500 | ₹3,041 |

| ₹10,000 / mo | ₹4,37,000 | ₹8,11,000 | ₹6,083 |

| ₹25,000 / mo | ₹10,93,000 | ₹20,27,500 | ₹15,206 |

| ₹50,000 / mo | ₹21,86,000 | ₹40,55,000 | ₹30,413 |

| ₹1,00,000 / mo | ₹43,72,000 | ₹81,10,000 | ₹60,825 |

Mutual Fund Agent Commission are made up of payments that go to agents or agencies, when they help to sell mutual funds. That forms a main part of how the industry about mutual funds works. The agents help investors choose right funds based on their targets in money and ability to handle risks.

DISCLOSURE: This post may contain affiliate links, meaning when you click the links and make a purchase, I receive a commission. As an Amazon Associate I earn from qualifying purchases.

They also care about the papers and lead the investors during the whole process.

How Mutual Fund Agent Commissions Work

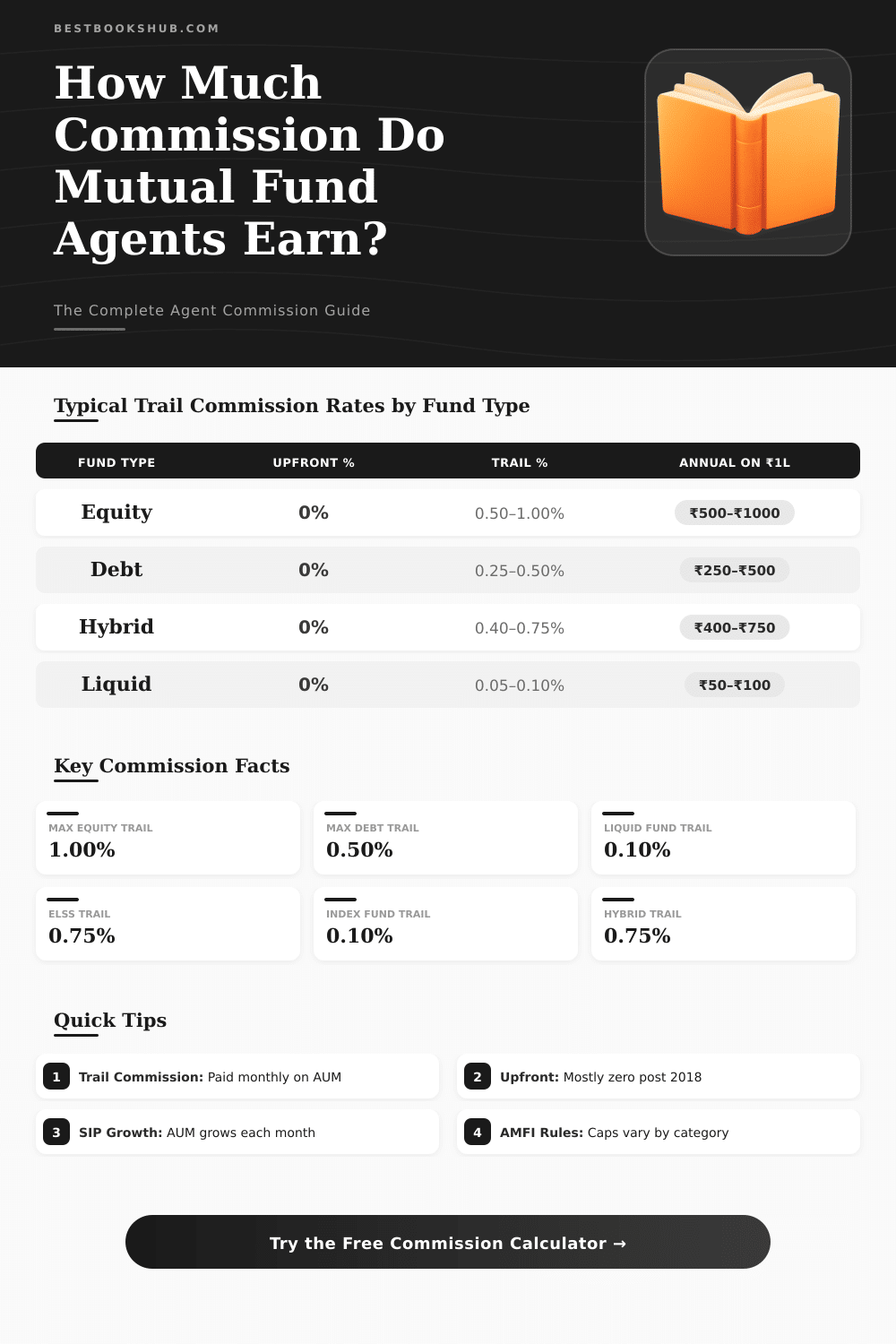

Agents receive three main kinds of commissions: prior, back and following. Suppliers of mutual funds offer various classes for investment, and those classes determine how one pays the commissions. A load is a one-time payment that some companies require during purchase or sale of certain mutual funds with a load base.

Agents usually receive Mutual Fund Agent Commission because of the sale of mutual funds, especially if the fund has a load.

Prior commissions appear only in certain situations, for instance during new fund offers or big investment. They do not repeat regularly. Rather, next commissions span while the investor stays in the fund.

The company takes part from the expense ratio for the agent fee. Those next payments commonly equal 0.5 percent of the investment yearly. Almost all companies about mutual funds give yearly next commission to the adviser of the company.

The commission hides at least partially. It sits in the output of that particular mutual fund. Some structures for pay are clear and announced, while others include secret commissions.

Investors do not pay commission directly, when they buy mutual funds by means of an agent ore agency.

Every mutual fund has now two versions. Direct mutual funds do not give commission to agents, so they own low expense ratio. Average funds have higher expense ratio, because the fee goes to the adviser.

Direct versions can give up to 1.5 percent more because of that absence. The commission for shares ranges between 0.40 and 1.70 percent, while for bonds it sits between 0.05 and 1 percent.

For instance, if someone places an order to buy a mutual fund in 20,000 dollars, the highest commission could reach 435 dollars plus 5.25 dollars for process and handling. In another example, investing 10,000 dollars through an agent like LPL, one could lose 550 dollars right off the top, so that only 9,450 dollars truly go in investment. Buying directly at companies like Fidelity or Vanguard, the whole 10,000 dollars stayinvested without any commission.

Sales based on commissions for mutual funds can create conflict of interests between the adviser and the client. Change to a setup based on fees, where advisers charge a percent of the values, is a good way. Thousands of American mutual funds are available without transaction fee, while others apply simple pricing structure.

Vanguard removed commissions for agents already in the 1970s, what meant lower costs and bigger returns for investors.